Network Tokenisation for Mastercard

Network Tokenisation Overview

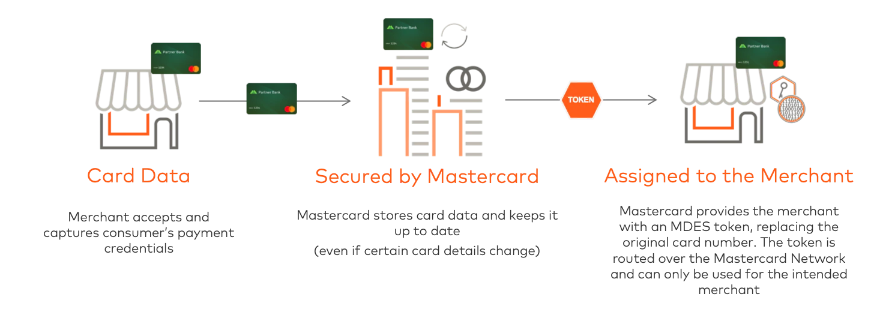

The difference with Network Tokenisation is that we (Ezypay) are swapping the real payment details (a PAN) with the card scheme (the network). We send Mastercard a PAN and a TRID (Token Requestor ID, similar to a Merchant ID or MID), and they give us back a token. That token is unique to both the card, and the Merchant, which makes the token really secure. There’s a security benefit to Network Tokenisation, particularly for companies who want to avoid the hassle of storing sensitive PAN data themselves, just like we take care of that complexity for our partners by collecting and storing card data and just providing them with a token.

When it is time to process a transaction, we pass the token to Mastercard, instead of the PAN. They then look up the corresponding PAN, and send the real payment details, along with the token, to the issuer for authorisation.

Benefits of Network Tokenisation

-

Network Tokenisation ensures better collection rate as credit or debit cards that has been misplaced or reported lost/stolen will still be allowed to transact (similar to an expired card scenario).

-

Network tokenisation helps increase the authorisation rate. The token is specific to the card and merchant, so there is a lower risk associated, hence less declines due to fraud.

What does an integrator needs to do to enable this capability?

There is nothing an integrator will need to do to enable network tokenisation into their payment capabilities. This is automatically enabled, as long as a payment is initiated via a MasterCard transaction (currently this feature is offered to Malaysia, Singapore and Australia). Ezypay is looking into expending this capabilities to other regions in the near future.

Updated 3 months ago